Built-in Studies Reference Guide

The following document outlines the technical analysis theory for popular built-in studies.

Table of contents

- Accumulation/Distribution (A/D)

- Accumulative Swing Index (ASI)

- ADX/DMS

- Alligator

- Anchored VWAP

- Aroon

- Aroon Oscillator

- Average True Range (ATR)

- ATR Bands

- ATR Trailing Stop

- Awesome Oscillator (Awesome)

- Balance of Power

- Beta

- Bollinger Bands®

- Bollinger Bandwidth

- Bollinger %B

- Center of Gravity (COG)

- Chaikin Money Flow (CMF)

- Chaikin Volatility

- Chande Forecast Oscillator (CFO)

- Chande Momentum Oscillator (CMO)

- Choppiness Index

- Commodity Channel Index (CCI)

- Coppock Curve

- Correlation Coefficient

- Darvas Box

- Depth of Market

- Detrended Price Oscillator

- Disparity Index (DI)

- Donchian Channel

- Donchian Width

- Ease of Movement (EOM)

- Ehler Fisher Transform (EFT)

- Elder Force Index

- Elder Impulse System

- Elder Ray Index

- Fractal Chaos Bands

- Fractal Chaos Oscillator

- Gator Oscillator (GO)

- GoNoGo Trend

- Gopalakrishnan Range Index (GAPO)

- Guppy Multiple Moving Average

- High Low Bands

- High Minus Low

- Highest High Value (HHV)

- Historical Volatility

- Ichimoku Cloud (intro)

- Intraday Momentum Index

- Keltner Channel

- Klinger Volume Oscillator

- Linear Regression Forecast

- Linear Regression Intercept (LR-I)

- Linear Regression R2

- Linear Regression Slope

- Lowest Low Value (LLV)

- Market Facilitation Index (MFI)

- Mass Index (MI)

- Median Price

- Momentum

- Money Flow Index

- Moving Average

- Moving Average Convergence/Divergence (MACD)

- Moving Average Cross

- Moving Average Deviation

- Moving Average Envelope

- Negative Volume Index

- On Balance (Cumulative) Volume (OBV)

- Option Sentiment by Strike

- Parabolic SAR

- Performance Index (PI)

- Pivot Points

- Positive Volume Index (PVI)

- Pretty Good Oscillator

- Price Momentum Oscillator (PMO)

- Price Oscillator

- Price Rate of Change

- Price Relative (Relative Strength)

- Price Volume Trend (PVT)

- Prime Number Bands (PNB)

- Prime Number Oscillator

- Pring’s Know Sure Thing (KST)

- Pring’s Special K

- Projected Aggregate Volume (PAV)

- Projected Volume at Time (PVAT)

- Psychological Line (PL)

- QStick

- Rainbow Moving Average (RMA)

- Rainbow Oscillator (RO)

- Random Walk Index (RWI)

- Rapid Adaptive Variance Indicator (RAVI)

- Relative Strength

- Relative Strength Index (RSI)

- Relative Vigor Index (RVI)

- Relative Volatility

- Schaff Trend Cycle (STC)

- Shinohara Intensity Ratio (SIR)

- Standard Deviation

- STARC Bands

- Stochastics

- Stochastic Momentum (SMI)

- Supertrend

- Swing Index (SI)

- Time Series Forecast

- Trade Volume Index (TVI)

- Trend Intensity Index (TII)

- TRIX Oscillator

- True Range (TR)

- Twiggs Money Flow (TMF)

- Typical Price (TP)

- Ulcer Index

- Ultimate Oscillator

- Valuation Lines

- Vertical Horizontal Filter (VHF)

- Volatility Cone

- Volume Chart

- Volume Oscillator (VO)

- Volume Profile

- Volume Rate of Change

- Volume Underlay

- Volume Weighted Average Price (VWAP)

- Vortex Indicator (VI)

- Weighted Close (WC)

- Williams %R

- ZigZag

Accumulation/Distribution (A/D)

Indicator Type

Trend Analysis, Money Flow

Description

The Accumulation/Distribution (A/D) indicator calculates the strength of the market over time, based on the net change in price for each period compared to its prior period. When the net change is positive, the maximum difference between the close and the low or the close and the prior close is added to the A/D. Conversely, if the net change is negative the maximum difference between the close and the high or the prior close is subtracted from the A/D.

You can use the A/D to analyze money flow. In this case, the positive or negative direction is multiplied by the volume for the current period.

Note: The A/D uses all the data loaded into the chart. Typically this is 200 bars prior to the first bar shown. As the chart is compressed or panned it will load more data forcing the A/D to recalculate and will produce different values. That said, the pattern of the A/D will remain the same.

Math

- Input Parameter

- Use Volume

- todayAD:

- if Close(i)>Close(i-1) then

todayAD(i)=Close(i)-min(Low(i),Close(i-1))

- else if Close(i)<Close(i-1) then todayAD(i)=Close(i)-max(High(i),Close(i-1))

- else todayAD(i)=0

- If user selects “Use Volume”: todayAD(i)=todayAD(i)*Volume(i)

- if Close(i)>Close(i-1) then

todayAD(i)=Close(i)-min(Low(i),Close(i-1))

- R(i) = todayAD(i)+todayAD(i-1)+todayAD(i-2)+…+TodayAD(1)

Accumulative Swing Index (ASI)

Indicator Type

Trend Analysis

Description

The Accumulative Swing Index indicator (ASI) aggregates all the prior Swing Index (SI) values providing a longer term tool to support a swing trading strategy. The ASI is designed to help simplify market interpretation and leverage the sensitivity of the SI which helps detect potential changes in trend.

Note: The ASI uses all the data loaded into the chart. Typically this is 200 bars prior to the first bar shown. As the chart is compressed or panned it loads more data forcing the ASI to recalculate and will produce different values. That said, the pattern of the ASI will remain the same.

The Accumulative Swing Index was developed by Welles Wilder.

Related Study: Swing Index

Math

- T = Limit Move Value; if not supplied, 99999

- A(i) = abs(High(i)-Close(i-1))

- B(i)=abs(Low(i)-Close(i-1))

- C(i)=abs(High(i)-Low(i))

- D(i)=abs(Close(i-1)-Open(i-1))

- K(i)=max(A(i),B(i))

- M(i)=max(C(i),K(i))

- r(i)=M(i)+D(i)/4

- if M=A then r(i)=r(i)-B(i)/2

- else if M=B then r(i)=r(i)-A(i)/2

- S(i)=(50*((Close(i)-Close(i-1))+(Close(i)-Open(i))/2+(Close(i-1)-Open(i-1))/4)/r(i))*K(i)/T

- Swing Index: R(i)=S(i)

- Accumulative Swing Index: R(i)=R(i-1)+S(i)

ADX/DMS

Indicator Type

Trend Analysis, Momentum Oscillator

Description

ADX (Average Directional Index) or DMS (Directional Movement System) uses Directional Movement (DM) calculations to identify trends and gauge the strength of those trends. Directional Movement (DM) is defined as the largest part of the current period’s price range that lies outside the previous period’s price range. Each period will either be positive (PDM = larger range above previous range), negative (NDM = larger range below previous range), or zero if moves above and below the previous period’s range are equal or price stays within the previous day’s range (an inside bar).

A smoothed average of both positive and negative directional movement are calculated and then divided by the Average True Range (ATR) to derive the Plus Directional Indicator (+DI) and Minus Directional Indicator (-DI). Each period will have only one result, either plus, minus or zero. +DI increases and -DI decreases during rising trends and vice-versa in down trends. The DI Difference (DI) is the sum of +DI and -DI. Accordingly, the DI Histogram will oscillate around zero as the market trends.

The Average Directional Index (ADX) is a simple moving average of the absolute value of the DI. The ADX is a non-directional trend analysis tool. Low values indicate the market has consolidated and is ready to trend, whereas high values indicate a strong trend has been well established and may be nearing an end.

The ADX/DMS study displays the ADX line as well as the +DI and -DI. In addition, there is an option to display a histogram of the spread between +DI and -DI which serves as a momentum oscillator.

Formula

-

Directional Movement (DM) is defined as the largest part of the current period’s price range that lies outside the previous period’s price range.

- PDM = current high minus the previous high (called plus DM)

- MDM = current low minus the previous low (called minus DM)

- If PDM > MDM then MDM is set to zero

- If MDM > PDM then PDM is set to zero

- If current range lies within or is equal to the previous range then set both PDM and MDM to zero

-

Calculate the value of the Plus and Minus Directional Indicators:

- PDI(n) = PDM(n) * 100 ÷ ATR(n)

- MDI(n) = MDM(n) * 100 ÷ ARR(n)

- Where: n = Number of periods

- ATR = Average True Range

-

Calculate the absolute value of the Directional Movement Index (DMI):

- DMI = (PDI – MDI) ÷ (PDI + MDI)

-

Calculate the Average Directional Movement (DMIA a.k.a. ADX):

- DMIA(n) = SMA of DMI

Math

- Input Parameters

- Period (N)

- Smoothing Period (Sm)

- Display Settings

- Series (Show/Hide)

- Shading (Show/Hide)

- Histogram (Show/Hide)

- Sm=N unless user specified, this is ADX Smoothing period

- TR(i)=True Range (max(High(i),Close(i-1))-min(Low(i),Close(i-1)))

- pDM(i)=max(0,High(i)-High(i-1))

- nDM(i)=max(0,Low(i-1)-Low(i))

- if pDM(i)>nDM(i), then nDM(i)=0

- if(nDM(i)>pDM(i), then pDM(i)=0

- if(pDM(i)=nDM(i), then pDM(i)=0 and nDM(i)=0

- if i<=N:

- spDM(i)=spDM(i-1)+pDM(i)

- snDM(i)=snDM(i-1)+nDM(i)

- sTR(i)=sTR(i-1)+TR(i)

- else:

- spDM(i)=spDM(i-1)-spDM(i-1)/N+pDM(i)

- snDM(i)=snDM(i-1)-snDM(i-1)/N+nDM(i)

- sTR(i)=sTR(i-1)-sTR(i-1)/N+TR(i)

- if i>=N:

- pDI(i)=100*spDM(i)/sTR(i)

- nDI(i)=100*snDM(i)/sTR(i)

- DX(i)=100*abs(pDI(i)-nDI(i))/(pDI(i)+nDI(i))

- if i=Sm+N-1:

- R(Sm+N-1)=(DX(Sm+N-1)+DX(Sm+N-2)+DX(Sm+N-3)+…+DX(Sm))/Sm

- else:

- R(i)=(R(i-1)*(Sm-1)+DX(i))/Sm

- Histogram: pDI(x) – nDI(x)

Alligator

Indicator Type

Moving Averages/Bands

Description

The Alligator indicator uses three smoothed moving averages (SMMAs) named Jaw, Teeth, and Lips. Each one is offset forward (into the future) to indicate convergence/divergence relationships. The SMMAs are calculated on the Median Price. When the market is trending, the Alligator lines will diverge. When the three lines are close together, the Alligator indicates consolidation. The Gator oscillator is often used as a companion study to better understand the divergence/convergence between the three SMMAs.

The Alligator study can hide its Jaw, Teeth, and Lips lines, enabling users to show only the Fractal Arrows to emphasize trading signals.

The Alligator indicator was invented by Bill Williams.

Related Study: Gator Oscillator (GO)

Formula

Calculate three moving averages and offset them into the future.

- The Jaw line a 13-period SMMA, moved by 8 bars into the future;

- The Teeth line is an 8-period SMMA, moved by 5 bars into the future;

- The Lips line is a 5-period SMMA, moved by 3 bars into the future.

Math

- Input Parameters

- Jaw Period (Nj)

- Jaw Offset (Oj)

- Teeth Period (Nt)

- Teeth Offset (Ot)

- Lips Period (Nl)

- Lips Offset (Ol)

- Display Settings

- Lines (Show/Hide)

- Fractals (Show/Hide)

- Alligator Results:

- Rj(i)=SMMA(i-Oj,MP,Nj) //MP=Median Price

- Rt(i)=SMMA(i-Ot,MP,Nt)

- Rl(i)=SMMA(i-Ol,MP,Nl)

- Alligator Fractals:

- High(i)>max(High(i-1), High(i-2), High(i+1), High(i+2))

- Low(i)<min(Low(i-1), Low(i-2), Low(i+1), Low(i+2))

Anchored VWAP

Indicator Type

Volume, Moving Averages/Bands

Description

Anchored VWAP derives the volume-weighted average price (VWAP) starting from a specified date and time. Unlike VWAP, the Anchored VWAP can be applied to both intraday and historical price data. The mean of the high, low, and close price is the default price used to derive Anchored VWAP.

Related Study: Volume Weighted Average Price (VWAP)

Math

See VWAP

Aroon

Indicator Type

Trend Analysis

Description

The Aroon indicator measures the strength of a trend based on the recency of new Highs/Lows. Aroon plots two lines: the Aroon Up is based on recent highs and Aroon Down is based on recent lows. The values shown are in percentage terms and fluctuate between 0 and 100.

Related Study: Aroon Oscillator

Formula

- Parameters: Period (n)

- Aroon Up = 100 x (n – Days Since n-day High)/n

- Aroon Down = 100 x (n – Days Since n-day Low)/n

Math

- Input Parameters

- Period (N)

- For i = 0 to N-1 find Highest High’s index and Lowest Low’s index

- Xdh = index of HHV(i+1,N) includes current bar

- Xdl = index of LLV(i+1,N) includes current bar

- Rup(i) = 100*(1-(i-xdh)/N)

- Rdn(i) =100*(1-(i-xdl)/N)

Aroon Oscillator

Indicator Type

Momentum Oscillator

Description

The Aroon Oscillator measures the difference between Aroon Up and Aroon Down. The Aroon Oscillator is bounded between 100 and -100.

Related Study: Aroon

Formula

-

Parameters: Period (n)

-

Aroon Oscillator = Aroon Up – Aroon Down

Math

- Input Parameters

- Period (N)

- For i=0 to N-1 find Highest High’s index and Lowest Low’s index

- xdh=index of HHV(i+1,N) includes current bar

- xdl=index of LLV(i+1,N) includes current bar

- Rup(i)=100*(1-(i-xdh)/N)

- Rdn(i)=100*(1-(i-xdl)/N)

- Rosc(i)=Rup(i)-Rdn(i)

ATR Bands

Indicator Type

Moving Averages/Bands

Description

The ATR Bands indicator displays two lines forming an envelope around the Price series (X) based on recent volatility as measured by Average True Range (ATR). The Bands are calculated using a ±Shift multiple of the ATR and added/subtracted from X. When the price breaks out of the channel, it can be interpreted as a signal.

Related Study: Average True Range (ATR), ATR Trailing Stop, True Range (TR)

Note: This study can be applied to other studies by using the Field parameter.

Formula

- Parameters: Period (N); %Shift

- Top Band = Median Band + %Shift * ATR(N)

- Bottom Band = Median Band - %Shift * ATR(N)

Math

- Input Parameters

- Period (N)

- Field (X) //Any value displayed on the chart

- Shift (S)

- Display Settings

- Channel Fill (On/Off)

- Rm(i) (median band) = X(i)

- Rt(i) (top band) = Rm(i)+(S*ATR(i))

- Rb(i) (bottom band) = Rm(i)-(S*ATR(i))

ATR Trailing Stop

Indicator Type

Support/Resistance, Volatility

Description

ATR Trailing Stop highlights a reversal in trend by plotting a stop point based upon recent market volatility. Average True Range (ATR) is used to adjust the stop point based upon recent market volatility. The trailing stop will continue to increase in a rising market, and decrease in a down market. If the trend stalls or the market consolidates, the stop will stabilize at a level until the trend resumes or crosses through the stop level. ATR Trailing Stop flips to the invert when price corrects below/above the stop line.

Calculate the ATR and then apply the multiplier. For an up trend, subtract from previous close. For a down trend, add to the previous close.

Related Study: Average True Range (ATR), ATR Bands, True Range (TR)

Formula

(See Average True Range)

Math

- Input Parameters

- Period (N)

- Multiplier (M)

- HighLow (On/Off)

- Display Settings

- Plot Type

- base(i) = Close(i-1)

- offset(i) = ATR(i-1)*M (M is user supplied)

- if Close(i-1)>R(i-1) and Close(i-2)>R(i-1):

- if using High/Low, base(i)=High(i-1)

- R(i)=max(R(i-1),base(i)-offset(i))

- else if Close(i-1)<=R(i-1) and Close(i-2)<=R(i-1):

- if using High/Low, base(i)=Low(i-1)

- R(i)=min(R(i-1),base(i)+offset(i))

- else if Close(i-1)>R(i-1):

- if using High/Low, base(i)=High(i-1)

- R(i)=base(i)-offset(i)

- else if Close(i-1)<=R(i-1):

- if using High/Low, base(i)=Low(i-1)

- R(i)=base(i)+offset(i)

Average True Range (ATR)

Indicator Type

Volatility

Description

The Average True Range (ATR) is a simple moving average of the volatility of the market as measured by the True Range (TR).

Related Study: ATR Bands, ATR Trailing Stop, True Range (TR)

Formula

ATR = SMA( True Range, n-period )

Math

-

Input Parameters

- Period (N)

-

TR(i) = True Range

-

R(i) = (R(i-1)*(N-1)+TR(i))/N

Awesome Oscillator (Awesome)

Indicator Type

Momentum Oscillator

Description

The Awesome Oscillator measures the difference between a 5 period simple moving average (SMA) and a 34 period SMA based on the median price of each bar. The result is an unbounded oscillator. The Awesome is displayed as a histogram and each value is colored based on if the Awesome value is increasing or decreasing to provide visual clarity.

Related Study: Price Oscillator

Math

-

MP = (Highest Price + Lowest Price)/2

-

ma1(i) = SMA(i,MP,5)

-

ma2(i) = SMA(i,MP,34)

-

R(i) = ma1(i) - ma2(i)

-

Data is displayed as histogram:

-

if R(i) > R(i-1) use INCREASING BAR color

-

if R(i) < R(i-1) use DECREASING BAR color

-

Balance of Power

Indicator Type

Momentum Oscillator

Description

The Balance of Power is a moving average of the internal strength of each bar. The internal strength is measured by deriving a ratio of each bar's close-open relative to its high-low range. The highest/lowest value for any bar 1/-1, which occurs if the market opens on the low and closes on the high, and vice-versa in a down market. If the close equals the open the value for the bar is zero, indicating the power is balanced between the bulls and the bears.

Math

-

Input Parameters

-

Period (N)

-

Moving Average Type (xMA)

-

-

R(i) = xMA(i,(Close-Open)/(High-Low),N)

Beta

Indicator Type

Volatility, Comparison

Description

Beta measures the volatility of returns for one security against those of a benchmark security, usually a market index. It is often used as a measure of risk of a security relative to the market. A Beta greater than 1.0 will tend to move up or down faster than the benchmark security.

Math

-

Input Parameters

-

Period (N)

-

Comparison Symbol (Comp)

-

-

BaseChg(i) = Close(i) ÷ Close(i-1)

-

CompChg(i) = Comp(i) ÷ Comp(i-1)

-

MABase(i) = SMA(i,BaseChg,N)

-

MAComp(i) = SMA(i,CompChg,N)

-

COVARn(i) = (BaseChg(i)-MABase(i)) * (CompChg(i)-MAComp(i))

-

VARn(i) = (BaseChg(i)-MABase(i))^2

-

R(i) = SMA(i,COVARn,N)/SMA(i,VARn,N)

Bollinger Bands®

Indicator Type

Moving Averages/Bands, Volatility

Description

The Bollinger Bands indicator displays two lines forming an envelope around a moving average of price. The upper and lower bands are determined by a number of standard deviations above and below the moving average. The expansion and compression of the bands highlight changes in volatility. Breakouts of the bands typically represent trading opportunities.

Bollinger Bands were created by John Bolinger.

Related Study: Bollinger Bandwidth, Bollinger %B

Note: This study can be applied to other studies by using the Field parameter.

Formula

-

Parameters: Period (N); Standard Deviations (S)

-

Middle Band = N-period moving average

-

Upper Band = N-period moving average + (N-period standard deviation of price x multiple)

-

Lower Band = N-period moving average – (N-period standard deviation of price x multiple)

Math

-

Input Parameters

-

Period (N)

-

Field (X)

-

Standard Deviations (S)

-

Moving Average Type (xMA)

-

-

Display Settings

- Channel Fill (On/Off)

-

Rm(i) (moving average) = xMA(i,X,N)

-

ts(i)=total shift=(S*STDEV(i,X,N,xMA)

Standard Deviation =

-

Calculate the average (mean) price for N periods

-

Subtract each price over N periods from the average price over N periods

-

Square each difference

-

Sum these squares

-

Divide this sum by N

-

Standard deviation = the square root of that number

-

-

Rt(i) (top band) = Rm(i)+ts(i))

-

Rb(i) (bottom band) = Rm(i)-ts(i))

Bollinger Bandwidth

Indicator Type

Volatility

Description

The Bollinger Bandwidth measures the difference (spread) between the upper and lower Bollinger Bands. As the market trends and price dispersion increases the bands will widen, thereby providing a measure of volatility. When the Bollinger Bandwidth is low, due to a market consolidation, it is often considered a setup for a trend.

Bollinger Bands were created by John Bolinger.

Related Study: Bollinger Bands®, Bollinger %B

Note: This study can be applied to other studies by using the Field parameter.

Formula

Bandwidth = (Upper Band – Lower Band) ÷ Central Moving Average * 100

Math

-

Input Parameters

-

Period (N)

-

Field (X) //Any value displayed on the chart

-

Standard Deviations (S)

-

Moving Average Type (xMA)

-

-

Rm(i) (median band) = xMA(i,X,N)

-

ts(i)=total shift=(S*STDEV(i,X,N,xMA)

-

Rt(i) (top band) = Rm(i)+ts(i))

-

Rb(i) (bottom band) = Rm(i)-ts(i))

-

Rw(i)=100*(Rt(i)-Rb(i))/ Rm(i) // can be represented as 200*ts(i)/Rm(i)

Bollinger %B

Indicator Type

Momentum Oscillator

Description

Bollinger %B is a percentage measure of a security’s location between the Bollinger Bands. %B can be lower than 0 or higher than 100 if price moves outside the bands which would be considered a breakout signal. A value of 50 implies the price is equal to the middle moving average.

Bollinger Bands were created by John Bolinger.

Related Study: Bollinger Bands®, Bollinger Bandwidth

Note: This study can be applied to other studies by using the Field parameter.

Formula

%B = (Price – Lower Band) ÷ (Upper Band – Lower Band)

Math

-

Input Parameters

-

Period (N)

-

Field (X) //Any value displayed on the chart

-

Standard Deviations (S)

-

Moving Average Type (xMA)

-

-

Display Settings

-

Overbought Threshold

-

Oversold Threshold

-

-

Rm(i) (median band) = xMA(i,X,N)

-

ts(i) (total shift) = (S*STDEV(i,X,N,xMA)

-

Rt(i) (top band) = Rm(i)+ts(i))

-

Rb(i) (bottom band) = Rm(i)-ts(i))

-

Rpb(i) = 50*(2*(Close(i)-Rm(i))/(Rt(i)-Rb(i))+1) // can be represented as ((Close(i)-Rm(i))/ts(i)+1)

Center of Gravity (COG)

Indicator Type

Momentum Oscillator

Description

The Center of Gravity (COG) is a leading oscillator created by John Ehlers in 2002. It is used to identify support and resistance. It is constructed using a weighted moving average, which according to its creator, was analogous to the weighted coordinates of an object’s mass distribution. It is accompanied by a Signal line.

Claiming to have zero lag, COG allows for clear indication of reversals due to the smoothing effect of the indicator. When the COG line crosses above the Signal line, it is an indication of an upturn. When the COG line crosses below the signal line, it is an indication of a market downturn.

Math

- Input Parameters

- Period (N)

- Field (X) //Any value displayed on the chart

- num(i) = 1*X(i)+2*X(i-1)+3*X(i-2)+…+N*X(i-N+1)

- den(i) = X(i)+X(i-1)+X(i-2)+…+X(i-N+1)

- R(i) = -num(i)/den(i)

Chaikin Money Flow (CMF)

Indicator Type

Money Flow

Description

The Chaikin Money Flow (CMF) indicator is a moving sum of volume which is weighted by where price closes within its range. The indicator oscillates around 0, with positive amounts indicating a bullish trend, and negative amounts indicating a bearish trend.

The weight is called a “multiplier”, which ranges from -1 for a close at the low to +1 for a close at the high. A multiplier of -1 implies all the volume is negative, and is subtracted from the moving sum. In contrast, if the multiplier equals +1, all the volume for the period is added to the moving sum.

The Chaikin Money Flow was developed by Marc Chaikin.

Related Study: On Balance (Cumulative) Volume (OBV), Twiggs Money Flow (TMF)

Formula

Money Flow Multiplier = ((Close–Low)–(High–Close)) / (High – Low)

Money Flow Volume = (Money Flow Multiplier) x Volume

CMF = (N-Period Sum of Money Flow Volume)/(N-Period Sum of Volume)

Math

- Input Parameters

- Period (N)

- MFV(i) = Volume(i)*(2*Close(i)-High(i)-Low(i))/(High(i)-Low(i))

- sMFV(i) = MFV(i)+MFV(i-1)+MFV(i-2)+…+MFV(i-N+1)

- sVol(i) = Volume(i)+Volume(i-1)+Volume(i-2)+…+Volume(i-N+1)

- R(i) = sMFV(i)/sVol(i)

Chaikin Volatility

Indicator Type

- Volatility

Description

Chaikin Volatility measures the rate of change, in percentage terms, of a moving average of the high-low range. Higher values indicate the volatility (as measured by range) has been increasing relative to itself. The values are unbounded.

The Chaikin Volatility was developed by Marc Chaikin.

Math

- Input Parameters

- Period (N)

- Rate of Change (ROC)

- Moving Average Type (xMA)

- ma(i) = xMA(i,High-Low,N)

- R(i) = 100*((ma(i)/ma(i-ROC))-1)

Chande Forecast Oscillator (CFO)

Indicator Type

Momentum Oscillator

Description

The Chande Forecast Oscillator (CFO) measures the spread, in percentage terms, between the market price and a Time Series Moving Average (TSMA) which is a n-period moving linear regression using the “least squares fit” method. The oscillator is above zero when the price is above the CFO and less than zero if it is below. The oscillator is quite responsive to changes in trend as the TSMA follows price quite closely.

The Chande Forecast Oscillator was introduced by Tushar Chande.

Related Study: Moving Average Deviation

Note: This study can be applied to other studies by using the Field parameter.

Math

- Input Parameters

- Period (N)

- Field (X) //Any value displayed on the chart

- T(i) = TSMA(i,X,N) //Time Series (TSMA)

- R(i) = 100*(1-T(i)/X(i))

Chande Momentum Oscillator (CMO)

Indicator Type

Momentum Oscillator

Description

The Chande Momentum Oscillator (CMO) compares, in percentage terms, the sum of all recent one-period price changes divided by the sum of the absolute values of the one-period price changes over the same time period. The range of the CMO is bounded between -100 and +100.

The Chande Momentum Oscillator was introduced by Tushar Chande and Stanley Kroll.

Math

- Input Parameters

- Period (N)

- Display Settings

- Show Zones (Show/Hide)

- OverBought

- OverSold

- mom(i) = Close(i)-Close(i-1)

- Sm(i) = mom(i)+mom(i-1)+mom(i-2)+…+mom(i-N+1)

- AbsSm = abs(mom(i))+abs(mom(i-1))+abs(mom(i-2))+…+abs(mom(i-N+1))

- R(i) = 100*Sm(i)/absSm(i)

Choppiness Index

Indicator Type

Trend Analysis, Volatility

Description

The Choppiness Index (CI) is a non-directional trend analysis indicator which rises during a consolidation and falls as the market trends. The CI is a bounded range between 0 - 100. The higher the value, the less the market is trending.

The Choppiness Index was created by Australian commodities trader E.W. Driess.

Math

- Input Parameters

- Period (N)

- Display Settings

- Show Zones (Show/Hide)

- OverBought

- OverSold

- sTR(i) = TR(i)+TR(i-1)+TR(i-2)+…+TR(i-N+1)

- hh = HHV(i+1,N) //Highest High starting at current bar

- ll = LLV(i+1,N) //Lowest Low starting at current bar

- R(i) = 100*ln(sTR(i)/(hh-ll))/ln(N)

Commodity Channel Index (CCI)

Indicator Type

Momentum Oscillator

Description

The Commodity Channel Index (CCI) study measures market momentum by deriving a price oscillator and normalizing it by the deviation of price from its average. Specifically, it uses the average of the high, low and close for the period (HLC3, also referred to as “typical price”) and subtracts the “n” period moving average of HLC3, this quantity is then divided by the mean deviation of price from the simple moving average (SMA). By measuring price relative to its SMA, the CCI effectively captures the acceleration and deceleration of a market trend.

CCI is an unbounded oscillator. A factor of 0.015 is used to center the series so that +100 and -100 (default threshold values) may be used to identify Overbought and Oversold conditions. When CCI equals 0 it indicates that price is equal to the SMA. The Commodity Channel Index was developed by Donald Lambert.

Formula

Typical Price = (high + low + close) ÷ 3

CCI = Typical Price (TP) – (n-period SMA of TP) ÷ (0.015 * Mean Deviation)

Mean Deviation = ∑ (absolute value of difference of TP and its N-pd SMA) ÷ N

Math

- Input Parameters

- Period (N)

- TP(i) = Typical Price

- a(i) = SMA(i,TP,N)

- md(i) = abs(TP(i)-a(i))+abs(TP(i-1)-a(i)) + abs(TP(i-2)-a(i))+…+abs(TP(i-N+1)-a(i))

- R(i) = N*(TP(i)-SMA(i,TP,N))/(.015*md(i))

Coppock Curve

Indicator Type

Momentum Oscillator

Description

The Coppock Curve is calculated by first summing two rate of change measures, one with a long period and second with a short period. The Coppock Curve is a weighted moving average of this sum.

The Coppock Curve was created by Edwin Coppock.

Note: This study can be applied to other studies by using the Field parameter.

Formula

-

Parameters: Short RoC Period, Long RoC Period, MA Period

-

RoCSum = 100 * ( (Short RoC) + (Long RoC) - 2 )

-

Coppock = WMA( RoCSum,N )

Math

- Input Parameters

- Period (N)

- Field (X) // Any value displayed on the chart

- Short RoC (N1)

- Long RoC (N2)

- s(i) = 100*((X(i)/X(i-N1)) + (X(i)/X(i-N2))-2)

- R(i)= WMA(i,s,N)

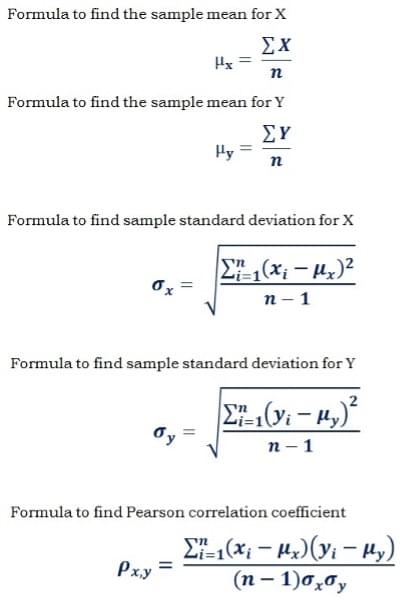

Correlation Coefficient

Indicator Type

Statistical, Relative performance measure, Comparison

Description

The Correlation Coefficient is a statistical measure used to calculate the strength and direction of the linear relationship (or the statistical relationship) between two data sets. For charting, it is between two traded instruments and the result is recalculated for each period in the same way a moving average “moves” through time using fresh data.

The value ranges between -1 to +1. The positive and negative correlation coefficient represents the direct (positive) and inverse (negative) linear correlation or statistical relationship between the data sets. That is, a positive correlation indicates two instruments have traded in the same direction, whereas a negative correlation implies they have traded in opposite directions. If the correlation is close to zero or equal to zero then the data sets are considered uncorrelated.

Formula

In the formula, the symbols μx and μy represent the mean of the two data sets X and Y respectively. The σx and σy represents the sample standard deviation of the two data sets X and Y respectively.

Step by Step Calculation:

- Find the sample mean μx for data set X.

- Find the sample mean μy for data set Y.

- Estimate the standard deviation σx for sample data set X.

- Estimate the sample deviation σy for data set Y.

- Find the covariance (cov(x, y)) for the data sets X and Y.

- Apply the values in the formula for correlation coefficient to get the result.

Math

- Input Parameters

- Comp=Close of the comparison symbol

- Period (N)

- sB(i)=Close(i)+Close(i-1)+Close(i-2)+…+Close(i-N+1)

- sC(i)=Comp(i)+Comp(i-1)+Comp(i-2)+…+Comp(i-N+1)

- sB2(i)=(Close(i)^2)+(Close(i-1)^2)+Close(i-2)^2)+…+Close(i-N+1)^2)

- sC2(i)=(Comp(i)^2)+(Comp(i-1)^2)+Comp(i-2)^2)+…+Comp(i-N+1)^2)

- sBC(i)=Close(i)*Comp(i)+Close(i-1)*Comp(i-1)+Close(i-2)*Comp(i-2)+…+Close(i-N+1)*Comp(i-N+1)

- vb=sB2(i)/N-((sB(i)/N)^2)

- vc=sC2(i)/N-((sC(i)/N)^2)

- cv=sBC(i)/N-sB(i)*sC(i)/(N^2)

- R(i)=cv/((vb*vc)^.5)

Darvas Box

Indicator Type

Support/Resistance

Description

The Darvas Box is a support/resistance indicator and a trading methodology rolled into one. It is an overlay study meant to indicate stocks that are trading at new highs by highlighting recent highs and lows to indicate entry points and placement of stop-losses.

The rules of drawing the Darvas Box are:

- Boxes are drawn around bars where an “all time high” was reached followed by 3 successive higher lows, and the high of the first bar was not broken by a higher high

- The box continues until either the original high is broken out, or the lowest of the 2 successive lows is broken below

- User can configure if high/low or close breaks the box

- User can configure if “Ghost boxes” are shown

- These will form on an upwards breakout of a Darvas

- The low of the Ghost box will be the same value as the high of the Darvas which was broken

- The height of the Ghost box will be the same as the Darvas box

- The width of the Ghost box will be either:

- The width of the Darvas box

- Until the Ghost box is broken below

- Until the Ghost box is broken above, in which case

- Another Ghost box forms with the lower left corner at the upper right corner of the preceding Ghost box

- User can define if arrow is drawn pointing to a volume spike and at what percentage that will be

- User can configure period defining all time high

- User can define a price minimum below which boxes will not form

- User can define whether “Stop Levels” are drawn and how far below the box low. Stop levels cannot be lowered, only raised (or broken).

While the indicator will run on any bar interval it is best used on higher intervals (i.e., weekly/monthly) with securities in a strong trend.

The logic behind the construction of the Darvas Box is somewhat complex but the usage is fairly straightforward. Once you have a closed box (a blue box assuming the default settings) you wait for a close (or a high) above the box on higher volume for a bullish signal or a close (or a low) below the box on higher volume for a bearish signal. The stop would generally be set just past the other side of the box. New boxes which form while you are in a trade provide an opportunity to build on a position upon a new breakout as well as updating a trailing stop level based on the most recent box. When used strictly as an indicator, the Darvas Box is an excellent mechanism to identify trading ranges on all bar intervals.

Depth of Market

Indicator Type

Volume

Detrended Price Oscillator

Indicator Type

Trend Analysis

Description

The Detrended Price Oscillator (DPO) seeks to remove trend information from the data. It does this by taking a moving average and shifting it to the left. It then subtracts the average from the time period from the close of that time period to arrive at the result.

The DPO will not be displayed on the most recent period as the moving average is shifted to the left. The resulting DPO plot will emphasize the movement of the security above and below the moving average while filtering out the general trends. The DPO is often used to help find cycles in the market by identifying peaks and troughs.

Note: This study can be applied to other studies by using the Field parameter.

Formula

The Moving Average type defaults to Simple, and the moving average period defaults to 14, computed on the Close.

N is the period, and X is the data field.

-

MA = xMA(i, X, N)

-

MAShifted = MA(i+int(N/2+1)) // where “int” is the whole number portion of the formula. For example, int(16.5)=16.

-

DPOi = Xi - MAShifted

Math

-

Input Parameters

-

Period (N)

-

Field (X) // Any value displayed on the chart

-

Moving Average Type (xMA)

-

-

R(i) = X(i)-xMA(i+int(N/2+1),X,N)

-

Moving average is shifted to the left

Disparity Index (DI)

Indicator Type

Momentum Oscillator

Description

The Disparity Index (DI) measures the distance of price from a moving average in percentage terms. The DI is an unbounded oscillator that uses percentage based calculation to normalize the spread across time and price.

Related Study: Moving Average Deviation

Note: This study can be applied to other studies by using the Field parameter.

Formula

- DI = Price ÷ Moving Average - 1

Math

-

Input Parameters

-

Period (N)

-

Field (X) // Any value displayed on the chart

-

Moving Average Type (xMA)

-

-

ma(i) = xMA(i,X,N)

-

R(i) = 100*(X(i)/ma(i)-1)

Donchian Channel

Indicator Type

Moving Averages/Bands

Description

The Donchian Channel displays a median line and bands that form an envelope around price. The Donchian High is the Highest High and the Donchian Low is the Lowest Low of the prior n periods starting with the previous bar. The median line is the average of the Donchian High and Donchian Low bands for each period.

The Donchian Channel was developed by Richard Donchian.

Related Study: Donchian Width, Highest High Value (HHV), Lowest Low Value (LLV)

Math

-

Input Parameters

-

High Period (Nh)

-

Low Period (Nl)

-

-

Display Setting

- Channel Fill (Show/Hide)

-

hh = HHV(i,Nh) // Highest High Value starts at previous bar

-

ll = LLV(i,Nl) // Lowest Low Value starts at previous bar

-

Rt(i) = hh

-

Rb(i) = ll

-

Rm(i) = (hh+ll)/2

Donchian Width

Indicator Type

- Volatility

Description

The Donchian Width indicator measures the spread between the Donchian High and Donchian Low bands. This serves as a simple measure of volatility as it captures the range expansion/compression of the market.

The Donchian Channel was developed by Richard Donchian.

Related Study: Donchian Bands, Highest High Value (HHV), Lowest Low Value (LLV)

Math

-

Input Parameters

-

High Period (Nh)

-

Low Period (Nl)

-

-

hh = HHV(i,Nh) // Highest High Value starts at previous bar

-

ll = LLV(i,Nl) // Lowest Low Value starts at previous bar

-

Rw(i) = hh-ll

Ease of Movement (EOM)

Indicator Type

- Money Flow, Trend Analysis, Momentum Oscillator

Description

The Ease of Movement (EOM) indicator is designed to measure volume’s impact on price. EOM first divides the volume by the period’s high-low Range, essentially distributing the volume equally across the high-low range. This value is then used as the denominator to measure the impact on the price change. A large change in price implies the volume was able to move the market.

EOM is an unbounded oscillator. A rising EOM indicates the market is easily moving upward, and the converse is true on the downside.

The Ease of Movement indicator was developed by Richard W. Arms, Jr.

Formula

EOM = Moving Average ( 1 bar Price Change ÷ ( Volume ÷ H-L Range ) )

Math

-

Input Parameters

-

Period (N)

-

Moving average Type (xMA)

-

-

ac(i) = (High(i)-Low(i))/2

-

ap(i) = (High(i-1)-Low(i-1))/2

-

dm(i) = ac(i)-ap(i) //Change in Midpoint

-

br(i) = (Volume(i)/100000000)/(High(i)-Low(i))

-

e(i) = dm(i)/br(i)

-

R(i) = xMA(i,e,N)

Ehler Fisher Transform (EFT)

Indicator Type

- Momentum Oscillator

Description

The Ehler Fisher Transform (EFT) is designed to convert prices into a Gaussian normal distribution based on the recent n-period trading range. The EFT is an unbounded oscillator with a trailing Trigger line that is the EFT with a lag of 1 period. The EFT is designed to reduce volatility of the indicator, but still provide timely signals of change in trend.

The Fisher Transform is a technical indicator created by John F. Ehlers

Math

-

Input Parameters

- Period (N)

-

hh=HHV(i+1,N) //Highest High starting at current bar

-

ll=LLV(i+1,N) //Lowest Low starting at current bar

-

n:

-

n(0)=0

-

n(i)=0.33*2*((((High(i)+Low(i))/2)-ll)/(hh-ll)-0.5)+0.67*n(i-1)

-

n(i)=min(max(n,-.9999),.9999)

-

-

R(i) = .5*ln((1+n)/(1-n))+.5*R(i-1)

-

Trigger(i) = R(i-1)

Elder Force Index

Indicator Type

- Money Flow, Momentum Oscillator

Description

The Elder Force Index (EFI) is a money flow based oscillator that multiplies the period’s volume times the price change thereby showing the strength of the price movement. EFI is an unbounded oscillator. A rising EFI indicates volume is driving prices higher, and a declining EFI indicates volume is pushing the market lower.

The Elder Force Index was developed by Alexander Elder.

Formula

-

Parameters: Period

-

EFI = EMA (Volume * 1 period Price Change, N-Period )

Math

-

Input Parameters

- Period (N)

-

EF1(i) = Volume(i)*(Close(i)-Close(i-1))

-

R(i) = EMA(i,EF1,N)

Elder Impulse System

Indicator Type

Trend Analysis

Description

The Elder Impulse System (EIS) combines net changes in an exponential moving average (EMA) of price with net changes in the MACD histogram to produce bullish and bearish signals applied to the chart using paintbars. The result is a colored bar chart where the colors represent bullish, bearish or neutral signals. Bullish (green) signals appear when the values of both the EMA and the MACD Histogram increase from the prior period. Conversely, if both decrease then it is a bearish (red) signal. If they move in opposite directions then it is a neutral signal (blue).

The Elder Impulse System was developed by Alexander Elder.

Formula

-

The study parameters in the EIS are fixed as follows:

-

EMA had a period of 13, computed on the Close.

-

The MACD has a fast period of 12, a slow period of 26, and a signal period of 9.

-

Math

-

ma(i) = EMA(i,Close,13)

-

cdh(i) = MACD(i,12,26,9) Histogram // This is the MACD-MACDSignal

-

if ma(i)>ma(i-1) and cdh(i)>cdh(i-1) then bullish

-

if ma(i)<ma(i-1) and cdh(i)<cdh(i-1) then bearish

-

display colored bar chart, bullish color if bullish, bearish color if bearish, otherwise neutral color

Elder Ray Index

Indicator Type

- Momentum Oscillator

Description

The Elder Ray Index is an unbounded oscillator that displays two superimposed histograms measuring the distance of the high/low from the exponential moving average.

The Elder Ray Index was developed by Alexander Elder.

Formula

-

Parameters: Period

-

Bull Power = High - EMA (Close, N-Period)

-

Bear Power = Low - EMA (Close, N-Period)

Math

-

Input Parameters

- Period (N)

-

Histogram1(i) = High(i) - EMA(i,Close,N)

-

Histogram2(i) = Low(i) - EMA(i,Close,N)

Fractal Chaos Bands

Indicator Type

- Moving Average/Bands, Trend Analysis

Description

The Fractal Chaos Bands are designed to identify breakouts and trend persistence based on the market making new Highs/Lows. An upside breakout is identified when the current high is the Highest High when compared to the prior two highs, in which case the Upper Band holds its last value and moves sideways. If the market is not trending, either up or down, then the Upper Band will display the high from two bars ago. The reverse is done for the Lower Band.

Related Study: Fractal Chaos Oscillator

Math

-

if High(i)<High(i-2) and High(i-1)<High(i-2) and going back, found 2 more Highs<High(i-2) before finding any>High(i-2) then

- Rh(i)=High(i-2)

-

if Low(i)>Low(i-2) and Low(i-1)>Low(i-2) and going back, found 2 more Lows>Low(i-2) before finding any<Low(i-2) then

- Rl(i)=Low(i-2)

Fractal Chaos Oscillator

Indicator Type

Momentum Oscillator

Description

The Fractal Chaos Oscillator has three states -1, 0, +1. A value of 0 indicates the market is consolidating. A value of +1 indicates a change in the upper range of the market, as best seen using the Upper Fractal Chaos Band. A value of -1 indicates a change in the lower range of the market, as best seen using the Lower Fractal Chaos Band.

The Fractal Chaos Oscillator was developed by E. W. Dreiss.

Related Study: Fractal Chaos Bands

Math

-

if High(i)<High(i-2) and High(i-1)<High(i-2) and going back, found 2 more Highs<High(i-2) before finding any>High(i-2) then

-

Rh(i)=High(i-2)

-

Rosc(i)=1

-

-

if Low(i)>Low(i-2) and Low(i-1)>Low(i-2) and going back, found 2 more Lows>Low(i-2) before finding any<Low(i-2) then

-

Rl(i)=Low(i-2)

-

Rosc(i)=-1

-

-

if neither of the two conditions above,

- Rosc(i)=0

Gator Oscillator (GO)

Indicator Type

Oscillator, Trend Analysis

Description

The Gator Oscillator (GO) is derived from the Alligator indicator. It plots two histograms in opposite directions that highlight the divergence/convergence between the three SMMAs used in the Alligator: Jaws, Teeth, and Lips. The positive histogram is the absolute value of the (Jaw - Teeth). The negative histogram is the absolute value of the (Teeth - Lips) multiplied by -1.

Green histogram bars indicate the averages are diverging, highlighting acceleration of the trend. Red bars indicate convergence of the averages showing the trend is losing strength. Compression of the histograms helps determine when a market is consolidating.

Although the GO can be used separately, it is most often combined with the Alligator as they complement each other in giving a more complete overview of current market conditions. The GO shows the absolute degree of convergence/divergence of the three moving averages plotted by Alligator study.

Related Study: Alligator

Formula

Calculate three moving averages and offsets them into the future.

- The Jaw line a 13-period Smoothed Moving Average (SMMA), moved into the future by 8 bars;

- The Teeth line is an 8-period Smoothed Moving Average (SMMA), moved by 5 bars into the future;

- The Lips line is a 5-period Smoothed Moving Average, moved by 3 bars into the future.

- Gator Hist_1 = ABS( SMMA(median price,Jaws) - SMMA(median price, Teeth) )

- Gator Hist_2 = -1*ABS( SMMA(median price,Teeth) - SMMA(median price, Lips) )

Math

- Input Parameters

- Jaw Period (Nj)

- Jaw Offset (Oj)

- Teeth Period (Nt)

- Teeth Offset (Ot)

- Lips Period (Nl)

- Lips Offset (Ol)

- Alligator Results:

- Rj(i) = SMMA(i-Oj,MP,Nj) //MP=Median Price

- Rt(i) = SMMA(i-Ot,MP,Nt)

- Rl(i) = SMMA(i-Ol,MP,Nl)

- Gator Results (Histogram):

- Rjt(i) = abs(Rj(i)-Rt(i)) //Jaw-Teeth

- Rtl(i) = -abs(Rt(i)-Rl(i)) //Teeth-Lips

- if Rjt(i)>Rjt(i-1) use INCREASING BAR color

- if Rjt(i)<Rjt(i-1) use DECREASING BAR color

- if Rtl(i)>Rtl(i-1) use DECREASING BAR color

- if Rtl(i)<Rtl(i-1) use INCREASING BAR color

GoNoGo Trend

Indicator Type

- Trend Analysis

Description

The GoNoGo Trend study colors the price action of any security according to the strength of its trend, making it simple to identify and interpret the current trend:

-

Bright Blue price bars indicate the strongest bullish environment.

-

Aqua bars are slightly less bullish; they often occur at the start of a new trend, or as a strong bullish trend begins to weaken.

-

Amber bars represent uncertainty, often appearing in the transition from bull trend to bear trend and vice versa.

-

Pink bars indicate a lower intensity bearish environment

-

Dark Purple bars are shown when the bearish trend intensifies.

The “Go” and “NoGo” labels on the chart mark transitions to bull or bear trends, respectively.

Math

- Proprietary to GoNoGo Charts

Gopalakrishnan Range Index (GAPO)

Indicator Type

Volatility

Description

The Gopalakrishnan Range Index (GAPO) measures the volatility of the market by measuring the natural log of the spread between the Highest High and Lowest Low over a given period which is then normalized by the natural log. When the GAPO is increasing the market is making new highs or lows relative to the lookback period.

Formula

-

Parameter: Period (N)

-

GAPO = Natural Log(Highest High - Lowest Low) ÷ Natural Log(N)

Math

-

Input Parameters

- Period

-

hh = HHV(i,N) – Highest High starting at previous bar

-

ll = LLV(i,N) – Lowest Low starting at previous bar

-

R(i) = ln(hh-ll)/ln(N) - ln is the natural log

Guppy Multiple Moving Average

Indicator Type

Moving Averages/Bands

Description

The Guppy Multiple Moving Average (GMMA) combines a group of six short-term exponential moving averages (EMA) and a group of six long-term EMAs. The multiple moving averages provide a “weight of the evidence” approach to identify changing trends, breakouts, and trading opportunities in the price of an asset.

The Guppy Multiple Moving Average was introduced by Daryl Guppy.

Formula

-

Short Term (Red Averages)

-

EMA(3)

-

EMA(5)

-

EMA(8)

-

EMA(10)

-

EMA(12)

-

EMA(15)

-

-

Long Term (Blue Averages)

-

EMA(30)

-

EMA(35)

-

EMA(40)

-

EMA(45)

-

EMA(50)

-

EMA(60)

-

High Low Bands

Indicator Type

Moving Averages/Bands, Statistical

Description

The High Low Bands are drawn a percentage or number of points above and below a triangular moving average of the selected field.

Related Study: Triangular Moving Average, Moving Average Envelope

Math

-

Input Parameters

-

Period

-

Field

-

Shift Percentage

-

-

Creates a plot of the TMA plus 2 bands ±S percentage off the Close from the TMA

High Minus Low

Indicator Type

Volatility

Description

High Minus Low measures the trading range of the bar.

Related Study: True Range (TR)

Math

- R(i) = High(i)-Low(i)

Highest High Value (HHV)

Indicator Type

Statistical, Band

Description

Identifies the highest price over a defined range, excluding the current bar in order to highlight if the current price is exceeding the recent Highest High.

Related Study: Lowest Low Value (LLV)

Math

-

Input Parameters

- Period

-

Does not include current bar

-

R(i)=max(X(i-1),X(i-2),X(i-3),…,X(i-N)) //start at previous bar

Historical Volatility

Indicator Type

Volatility, Statistical

Description

Historical Volatility measures the standard deviation of the underlying percent returns over n-periods. The result is annualized.

Math

-

Input Parameters

-

Period (N)

-

Field (X) //Any value displayed on the chart

-

Days Per Year: Select 365 or 252 for Market Days in year for daily charts. For monthly charts there are 12 periods. For weekly charts 52 periods.

-

Standard Deviations (M)

-

-

AF = 100*(Number Periods in Year ^ .5)*M //Annualization Factor

-

L(i) = ln(X(i)/X(i-1))

-

avgL(i) = (L(i)+L(i-1)+L(i-2)+…+L(i-N+1))/N

-

d2(i) = ((L(i)-avgL(i))^2)+((L(i-1)-avgL(i))^2)+((L(i-2)-avgL(i))^2)+…+((L(i-N+1)-avgL(i))^2)

-

R(i) = ((d2(i)/N)^.5)*AF

Ichimoku Cloud

Indicator Type

Trend analysis, Support/Resistance

Description

The Ichimoku Cloud study is designed to indicate support/resistance, momentum, and trend direction. It plots five lines and computes various “clouds” based on the interactions between these lines. Ichimoku translates to “one look,” implying that the indicator can signal support and resistance at a glance.

There are five components:

- Tenkan Sen (Conversion Line) – Calculated as the sum of the Highest High over the past nine periods and the Lowest Low divided by two.

- The Kijun Sen (Base Line) – Calculated as the sum of the Highest High over the past 22 periods and the Lowest Low divided by two.

- Senkou Span A (leading) – The sum of the Tenkan Sen and the Kijun Sen divided by two. The calculation is then plotted 26 time periods ahead of the current price action.

- Senkou Span B (leading) – The sum of the Highest High and the Lowest Low over the past 52 periods divided by two. It is also plotted 26 periods ahead.

- Chikou (lagging) – The same and Senkou Span B leading but plotted 26 periods in the past.

Math

- 5 lines are drawn

- Conversion Line:

- Ncl=Conversion Line Periods

- Rcl(i)=(HHV(i+1,Ncl)+LLV(i+1,Ncl))/2 – include current period

- Base Line:

- Nbl=Base Line Periods

- Rbl(i)=(HHV(i+1,Nbl)+LLV(i+1,Nbl))/2 – include current period

- Lagging Span:

- Nlg=Lagging Span Periods

- Rlg(i)=Close(i-Nlg)

- Leading Spans:

- Nld=Leading Span Periods

- Rlda(i+Nld)=(Rcl(i)+Rbl(i))/2

- Rldb(i+Nld)=(HHV(i+1,Nld)+LLV(i+1,Nld))/2 – include current period

- “Clouds” are drawn between the Leading Spans as follows:

- Red cloud if Rldb(i)>Rlda(i)

- Green cloud if Rlda(i)>Rldb(i)

Intraday Momentum Index

Indicator Type

Momentum Oscillator

Description

The Intraday Momentum Index (IMI) measures trend strength by using a ratio of the moving sum of the close-open (candle body) over the past “n” periods and relative to the moving sum of the net decreases. The result is a bounded oscillator that is indexed between 0 and 100 and is displayed with Overbought (OB) and Oversold (OS) levels.

The methodology to calculate IMI is quite similar to the Relative Strength Indicator (RSI) and can be interpreted in a similar manner. The central difference between the two is IMI measures market strength/weakness using the range of close-open (hence, the use of ‘Intraday’ in the name) whereas RSI measures the one-period net change. An advantage of IMI is it tends to trend more smoothly and produces OB/OB levels more frequently.

Related Study: Relative Strength Index (RSI)

Math

-

Input Parameters

- Period (N)

-

Display Settings

-

Show Zones (On/Off)

-

OverBought

-

OverSold

-

-

d(i) = Close(i)-Open(i) //Candle body

-

p(i): max(0,d(i))

-

n(i): min(0,d(i))

-

totP(i) = totP(i-1)+totP(i-2)+totP(i-3)+…+totP(i-N+1)+p(i) //Sum of gains

-

totL(i) = totL(i-1)+totL(i-2)+totL(i-3)+…+totL(i-N+1)-n(i) //Sum of losses

-

R(i) = 100*(totP(i)/(totP(i)+totL(i))) //percent of point up vs losses

Keltner Channel

Indicator Type

Moving Averages/Bands

Description

The Keltner Channel indicator displays two lines forming an envelope around a moving average of price. The upper and lower channel lines are determined by adding/subtracting a multiple of the Average True Range above and below the moving average of price. The Keltner Channel highlights the expansion and compression of volatility.

Formula

-

Center Line: 50-day EMA

-

Upper Channel Line: 50-day EMA + (5 x ATR (10-period))

-

Lower Channel Line: 50-day EMA – (5 x ATR (10-period))

Math

- Input Parameters

- Period (N)

- Shift (%S)

- Moving Average Type (xMA)

- Display Settings

- Channel Fill (On/Off)

- Rm(i) = xMA(i,Close,N) //center line

- Rt(i) = Rm(i)+(%S*ATR(i)) //top channel

- Rb(i) = Rm(i)-(%S*ATR(i)) //bottom channel

Klinger Volume Oscillator

Indicator Type

Money Flow

Description

The Klinger Volume Oscillator (KVO) is designed to identify short term fluctuations in money flowing in or out of a security. Each period’s volume is assigned a positive or negative value based on the one period change in Typical Price (the mean of the high, low, and close). The KVO is the spread between a long and a short exponential moving average (EMA) of the directional volume series.

The Signal Line is simply an EMA of the KVO line. The KVO Histogram measures the spread between the KVO and the Signal line. The KVO Histogram is colored green when the values are increasing and red when they are decreasing (green and red are default colors).

KVO is useful in helping evaluate if volume is supporting the trend.

The KVO was developed by Stephen Klinger.

Formula

UpDnVol = directional change in HLC3 * Volume

KVO = EMA(UpDnVol,n-bars) - EMA(UpDnVol,m-days)

Signal line = EMA of KVO

Histogram = KVO - Signal

Math

- Input Parameters

- Signal Periods (N3)

- Short Cycle (N2)

- Long Cycle (N1)

- TP(i) = Typical Price //HLC3

- s: if TP(i) >= TP(i-1), s=1; else s=-1

- SV(i) = Volume(i)*s //Negative or Positive Volume based on Net change in TP

- Long(i) = EMA(i,SV,N1)

- Short(i) = EMA(i,SV,N2)

- R(i) = Long(i)-Short(i)

- Signal(i) = EMA(i,R,N3)

- Histogram(i) = R(i)-Signal(i)

Linear Regression Forecast

Indicator Type

Statistical, Moving Averages/Bands

Description

The Linear Regression Forecast (LRF) uses the ordinary least squares method to derive a linear function which plots a straight line through prices so as to minimize the distances between the prices and the resulting trendline. The last point of the trendline is the forecasted value. The LRF is a moving series which plots the forecasted value of the derived trend line each period, thereby following the market like a moving average.

Related Study: Time Series Forecast, Linear Regression R2, Linear Regression Slope, Linear Regression Intercept (LR-I)

Note: This study can be applied to other studies by using the Field parameter.

Math

- Input Parameters

- Period (N)

- Field (F)

- SC(i) = X(i)+X(i-1)+X(i-2)+…+X(i-N+1)

- SWC(i) = N*X(i)-SC(i-1)

- SW = N*(N+1)/2

- b(i) = (N*SWC(i)-SW*SC(i))/(N*(SW^3)*(2*N+1)/3)

- a(i) = (SC(i)-b(i)*SW)/N

- Rf(i) = a(i)+b(i)*N //Forecast

Linear Regression Intercept (LR-I)

Indicator Type

Statistical, Moving Averages/Bands

Description

The Linear Regression Intercept (LR-I) uses the ordinary least squares method to derive a linear function which plots a straight line through prices so as to minimize the distances between the prices and the resulting trendline. The LR-I is a moving linear regression which plots the y-axis intercept for the derived trend line at each period. The intercept is the origination point of the regression and thereby appears to be an offset moving average.

Related Study: Linear Regression Forecast, Linear Regression Slope, Linear Regression Intercept (LR-I)

NOTE: This study can be applied to other studies by using the Field parameter.

Math

- Input Parameters

- Period (N)

- Field (F)

- SC(i) = X(i)+X(i-1)+X(i-2)+…+X(i-N+1)

- SWC(i) = N*X(i)-SC(i-1)

- SW = N*(N+1)/2

- b(i) = (N*SWC(i)-SW*SC(i))/(N*(SW^3)*(2*N+1)/3)

- a(i) = (SC(i)-b(i)*SW)/N

- Ri(i) = a(i) //Intercept

Linear Regression R2

Indicator Type

Statistical, Trend Analysis

Description

The Linear Regression R2 (LR-R2) uses the ordinary least squares method to derive a linear function which plots a straight line through prices so as to minimize the distances between the prices and the resulting trendline. The LR-R2 is a moving linear regression which plots the R-Squared for the derived trend line at each period. The LR-R2 is an oscillator that effectively measures the quality of fit of the derived trend line. Higher R2 values indicate better quality of fit of the trend line and the LR-Forecast thereby making it an ideal companion study to LR-Forecast.

Related Study: Linear Regression Forecast, Linear Regression Intercept (LR-I), Linear Regression Slope

Note: This study can be applied to other studies by using the Field parameter.

Math

- Input Parameters

- Period (N)

- Field (X)

- SC(i) = X(i)+X(i-1)+X(i-2)+…+X(i-N+1)

- SWC(i) = N*X(i)-SC(i-1)

- SW = N*(N+1)/2

- b(i) = (N*SWC(i)-SW*SC(i))/(N*(SW^3)*(2*N+1)/3)

- a(i) = (SC(i)-b(i)*SW)/N

- c(i) = ((N-1)*(SW^2)/(N-1)*(SC(i)^2)

- Rr2(i) = (b(i)^2)*c(i) //R2 (RSquared)

Linear Regression Slope

Indicator Type

Statistical, Momentum Oscillator

Description

The Linear Regression Slope (LR-Slope) uses the ordinary least squares method to derive a linear function which plots a straight line through prices so as to minimize the distances between the prices and the resulting trendline. The LR-Slope is a moving linear regression which plots the slope for the derived trend line at each period. The LR-Slope is an oscillator that effectively measures the direction of the market over the defined period.

Related Study: Linear Regression Forecast, Linear Regression Intercept (LR-I), Linear Regression R2

Note: This study can be applied to other studies by using the Field parameter.

Math

- Input Parameters

- Period (N)

- Field (X)

- SC(i) = X(i)+X(i-1)+X(i-2)+…+X(i-N+1)

- SWC(i) = N*X(i)-SC(i-1)

- SW = N*(N+1)/2

- b(i) = (N*SWC(i)-SW*SC(i))/(N*(SW^3)*(2*N+1)/3)

- a(i) = (SC(i)-b(i)*SW)/N

- c(i) = ((N-1)*(SW^2)/(N-1)*(SC(i)^2)

- Rs(i) = b(i) //Slope of trendline

Lowest Low Value (LLV)

Indicator Type

Statistical, Band

Description

Identifies the lowest price over a defined range, excluding the current bar to highlight if the current price is below the recent Lowest Low.

Formula

LLV = Lowest low within the range

Math

- Input Parameters

- Period (N)

- Does not include current bar

- R(i) = min(X(i-1),X(i-2),X(i-3),…,X(i-N)) // start at previous bar

Market Facilitation Index (MFI)

Indicator Type

Money Flow, Volatility

Description

The Market Facilitation Index (MFI) is a histogram that analyzes the effect of volume on price. The MFI does not provide directional information, but rather divides the bars range by volume thereby measuring if price responded to the volume executed. A high MFI indicates the volume was able to drive price movement, whereas a low MFI indicates significant balance between buyers and sellers.

The MFI histogram is colored to identify four states that indicate the quality of the price action in relation to increasing or decreasing volume:

-

Green: MFI and volume both increased, signifying the directional momentum is increasing and the volume was able to move price.

-

Fade (Brown): MFI and volume both decreased, signifying momentum is decreasing.

-

Fake (Blue): MFI is increasing while volume is decreasing, signifying uncertainty about whether one-off speculators are driving the market or not

-

Squat (Pink): MFI is decreasing while volume is increasing, signifying active competition between the bears and bulls in the market, and unclear price direction.

The MFI was developed by Bill Williams.

Math

- Input Parameters

- Scale Factor (SF) //normalization factor for end user

- R(i) = SF*(High(i)-Low(i))/Volume

- Data is displayed as a histogram with 4 colors:

- if R(i)>R(i-1) and Volume(i)>Volume(i-1) use GREEN color

- if R(i)>R(i-1) and Volume(i)<Volume(i-1) use FAKE color

- if(R(i)<R(i-1) and Volume(i)>Volume(i-1) use SQUAT color

- if(R(i)<R(i-1) and Volume(i)<Volume(i-1) use FADE color

Mass Index (MI)

Indicator Type

Volatility

Description

The Mass Index (MI) is a measure of volatility which has been stabilized to provide comparable values over time. High volatility is often associated with turning points in a market. When the MI crosses above the Bulge Threshold it is an indication that volatility has hit an extreme level.

The MI is derived by comparing an exponential moving average (EMA) of the high-low range to a smoothed EMA of the range. These ratios are then summed over time which serves to normalize the MI.

The Mass Index indicator was developed by Donald Dorsey.

Formula

MI = Sum of (EMA( HL Range,9 ) ÷ EMA ( EMA( HL Range,9 ),9 ), n-bars)

Math

-

Input Parameters

- Period (N)

-

Display Settings

- Bulge Threshold

-

E1(i) = EMA(i,High-Low,9)

-

E2(i) = EMA(i,E1,9) //Double EMA of Range

-

R(i) = E1(i)/E2(i) + E1(i-1)/E2(i-1) + E1(i-2)/E2(i-2) + E1(i-3)/E2(i-3) + ... + E1(i-N+1)/E2(i-N+1)

Median Price

Indicator Type

Moving Averages/Bands, Statistical

Description

A simple moving average of the mid-point between the High and Low of each bar.

Related Study: Moving Average

Math

-

Input Parameters

- Period (N)

-

X(i) = (High(i)-Low(i))/2

-

R(i) = (X(i)+X(i-1)+X(i-2)+…+X(i-N+1))/N

Momentum

Indicator Type

Momentum Oscillator

Description

Momentum measures the change in price over a set range, it is simply: Current Price – Price n-periods ago. Momentum is similar to Price Rate of Change except it shows actual change rather than percent change.

Formula

Momentum = Close - Close(N periods back)

Math

-

Input Parameters

- Period (N)

-

R(i) = X(i)-X(i-N) //Offset setting available as feature in code

Money Flow Index

Indicator Type

Money Flow, Momentum Oscillator

Description

Money Flow Index (MFI) is essentially a volume-weighted Relative Strength Index (RSI). However, instead of using simple close prices, MFI uses the Typical Price (TP or HLC3, the mean of the high, low and close) multiplied by volume. The result is then used in the RSI calculation as a ratio of average volume weighted size of the up-closes over the past “n” periods and compared to the average volume weighted size of the down-closes. The result is a bounded oscillator that ranges from 0 and 100.

The Money Flow Index (MFI) was developed by Gene Quong and Avrum Soudack.

Formula

Calculate Money Flow = Typical Price x Volume

Find positive money flow = sum of the volume weighted “up” typical price changes for the past n-periods

Find negative money flow = sum of the volume weighted “down” typical price changes for the past n-periods

Calculate Money Flow ratio = (n-period positive Money Flow)/ (n-period negative Money Flow)

Calculate Money Flow Index = 100 – 100/ (1 + Money Flow Ratio)

Math

- Input Parameters

- Period (N)

- RMF(i) = TP(i)*Volume(i) // TP = Typical Price (HLC3)

- If TP(i)-TP(i-1) > 0

- pMF(i)=RMF(i)+RMF(i-1)+RMF(i-2)+…+RMF(i-N+1) //sum of positive RMF values

- Else, nMF(i)=RMF(i)+RMF(i-1)+RMF(i-2)+…+RMF(i-N+1) //sum of negative RMF values

- R(i) = 100-100/(1+(pMF(i)/nMF(i)))

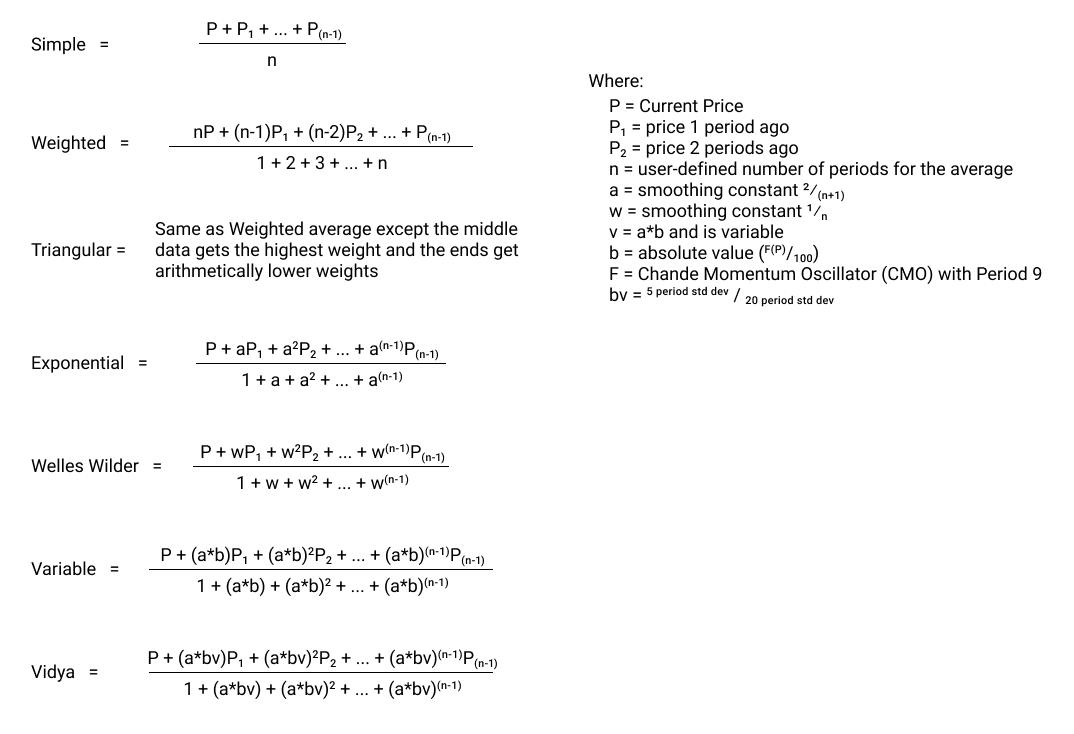

Moving Average

Indicator Type

Moving Averages/Bands

Description

Moving Averages are the most common tool to remove the noise and volatility from a data series allowing the underlying trend to be seen. They are a core component of many oscillators and other studies. Moving Averages may be applied to any data series or study shown on the chart using the “Field” parameter.

The Moving Average study supports eleven algorithms which increase/decrease the sensitivity of the study, often focusing on more recent data as follows:

-

Simple (SMA): mean (average) of the data.

- R(i)=(X(i)+X(i-1)+X(i-2)+…+X(i-N+1))/N

-

Double Exponential (DEMA)

- R(j)=2*EMA(i,X,N) - EMA(i,EMA(i,X,N),N)

-

Exponential (EMA): newer data are weighted more heavily geometrically.

-

m=2/(N+1)

-

if number of points < N, R(i)=SMA(i,X,number of points)

-

R(i)=m*X(i)+(1-m)*R(i-1)

-

-

Hull (HMA)

-

N’=N/2 rounded up to nearest whole number

-

N’’=sqrt(N) rounded down to nearest whole number

-

MMA(i)=2*WMA(i,X,N’)-WMA(i,X,N)

-

R(i)=WMA(i,MMA,N’’)

-

-

Time Series (TSMA): Calculates a linear regression trendline using the “least squares fit” method.

-

Part of the Linear Regression series, it’s the same as the Forecast

-

SC(i)=X(i)+X(i-1)+X(i-2)+…+X(i-N+1)

-

SWC(i)=N*X(i)-SC(i-1)

-

SW=N*(N+1)/2

-

b(i)=(N*SWC(i)-SW*SC(i))/(N*(SW^3)*(2*N+1)/3)

-

a(i)=(SC(i)-b(i)*SW)/N

-

R(i)=a(i)+b(i)*N

-

-

Triangular (TMA): This is a double SMA. Weighted average where the middle data are given the most weight, decreasing linearly to the end points.

-

N’=N/2 rounded up

-

a(i)=SMA(i,X,N’)

-

If N is even, N’’=N’+1 else N’’=N’

-

R(i)=SMA(i,a,N’’)

-

-

Triple Exponential (TEMA)

- R(j)=3*EMA(i,X,N) - 3*EMA(i,EMA(i,X,N),N) + 3*EMA(i,EMA(i,EMA(i,X,N),N),N)

-

Variable (VMA): An EMA with a volatility index factored into the smoothing formula. The Variable Moving average uses the Chande Momentum Oscillator as the volatility index.

-

Like Welles Wilder, except m= α*β and is variable

-

α=2/(N+1)

-

F=Chande Momentum Oscillator (CMO) with Period 9

-

β=abs(F(i)/100)

-

R(i)=α*β*X(i)+(1-(α*β))*R(i-1)

-

-

VIDYA/Variable Index Dynamic (VDMA): An EMA with a volatility index factored into the smoothing formula. The VIDYA moving average uses the Standard Deviation as the volatility index. (Volatility Index DYnamic Average)

-

Same as VMA except β is different

-

α=2/(N+1)

-

F1(i)=STDEV(i,X,5,SMA) – 5 period Standard Deviation of SMA

-

F2(i)=SMA(i,F1,20) – 20 period SMA of the 5 period STDEV

-

β= F1(i)/F2(i)

-

R(i)=α*β*X(i)+(1-(α*β))*R(i-1)

-

-

Weighted (WMA): newer data are weighted more heavily arithmetically.

-

Most recent data is given most weight, in linear fashion

-

R(i)=N*X(i)+(N-1)*X(i-1)+(N-2)*X(i-2)+…+2*X(i-N+2)+X(i-N+1)

-

-

Welles Wilder (Smoothed, SMMA): The standard EMA formula converts the time period to a fraction using the formula EMA% = 2/(n + 1) where n is the number of days. For example, the EMA% for 14 days is 2/(14 days +1) = 13.3%. Wilder, however, uses an EMA% of 1/14 (1/n) which equals 7.1%. This equates to a 27-day EMA using the standard formula.

-

Same as Exponential except for m:

-

m=1/N

-

R(i)=m*X(i)+(1-m)*R(i-1)

-

- or -

-

R(i)=(X(i)+(N-1)*R(i-1))/N

-

Smoothed Moving Average – Same calculation as an EMA except the smoothing constant is different.

-

P + wP1 + w2P2 + … + w(n-1)P(n-1)

-

1 + w + w2 + … + w(n-1)

-

Exponential smoothing constant: 2/(n+1)

-

Wilder smoothing constant: 1/n

-

Therefore, the Wilder average reacts slower than an exponential average. Also, the Wilder average can be converted into an exponential average with the formula 2n-1. For example, a 26-day Wilder average will draw the exact same plot as a 51-day exponential average.

-

-

Math

Moving Average Convergence/Divergence (MACD)

Indicator Type

Momentum Oscillator

Description

The Moving Average Convergence/Divergence (MACD) indicator makes use of three exponential moving averages (EMA). Two are averages of price and the third is a signal line that is an average of the difference of the other two.

The MACD line is generated from the first two averages, subtracting the longer from the shorter. The Signal Line is simply an EMA of the MACD line. The MACD Histogram measures the spread between the MACD and the Signal line. Changes in direction of the MACD Histogram are often used as early signals of change in trend.

Formula

-

MACD line – short moving average minus long moving average

-

Signal line – a moving average of the MACD line

-

Histogram – measures the difference between the MACD line and the Signal line

Math

- Input Parameters

- Fast MA Period (N2)

- Slow MA Period (N1)

- Signal Period (N3)

- Slow(i) = xMA1(i,X,N1)

- Fast(i) = xMA1(i,X,N2)

- R(i) = Fast(i)-Slow(i)

- Signal(i) = xMA2(i,R,N3)

- Histogram(i) = R(i)-Signal(i)

Moving Average Cross

Indicator Type

- Averages/Bands, Trend Analysis

Description

- Applies three moving averages of the same type to signal changes in trend as the shorter moving averages cross the longer ones.

Math

- See Moving Average

Moving Average Deviation

Indicator Type

Momentum Oscillator

Description

The Moving Average Deviation measures the spread, in points, between the market price and a moving average. The calculation may be shown in either points or percentages.

Related Study: Disparity Index (DI)

Note: This study can be applied to other studies by using the Field parameter.

Math

- Input Parameters

- Period (N)

- Field (X) // Any value displayed on the chart

- Moving average Type (xMA)

- Points or Percent

- MA(i) = xMA(i,X,N)

- R(i) = X(i)-MA(i) if output requested in points

- R(i) = 100*(X(i)/MA(i)-1) if output requested in percentage

Moving Average Envelope

Indicator Type

Moving Average/Bands

Description

The Moving Average Envelope (MAE) plots two lines that form an envelope around a Moving Average of price. The upper and lower bands are a percentage or number of points above and below the moving average.

The MAE can be derived using any of the eleven averaging methodologies supported and may be applied to any data field or study displayed on the chart.

Formula

-

For percentage envelopes:

- Upper band = moving average + x%(moving average)

- Lower band = moving average – x%(moving average)

-

For points envelopes:

- Upper band = moving average + constant

- Lower band = moving average – constant

Math

- Input Parameters

- Period (N)

- Field (X) //Any value displayed on the chart

- Shift Type (Percent or points)

- Shift (S)

- Moving Average Type (xMA)

- Display Settings

- Channel Fill (On/Off)

- %S=percentage shift, pS=point shift

- Rm(i) (median band) = xMA(i,X,N)

- Rt(i) (top band) = Rm(i)+(%S*X(i) + pS) //either %S or pS will be 0

- Rb(i) (bottom band) = Rm(i)-(%S*X(i) + pS)

Negative Volume Index

Indicator Type

Trend Analysis

Description

The Negative Volume Index (NVI) and its sister study, the Positive Volume Index (PVI), are designed to measure the quality of the trend by using volume as a barometer to evaluate the strength of the price action. Price changes on decreasing volume are considered a positive indicator. Whereas, price changes with increasing volume are considered a negative indicator, as increasing trading volumes are more common with retail traders following-the-crowd.

NVI is a moving average of cumulative percentage price changes on periods when volume decreases from bar to bar. For clarity, volume is only used to determine which data points to average, it is not part of the calculation. A trailing moving average of the NVI is used to signal significant changes in trend.

The Negative Volume Index (NVI) was developed by Paul Dysart.

Related Study: Positive Volume Index (PVI)

Note: This study can have other studies applied to it using the Field parameter.

Math

- Input Parameters

- Period (N)

- Field (X) // Any value displayed on the chart

- Moving Average Type (xMA)

- If Volume(i) < Volume(i-1) // negative change in volume

- t(i) = t(i-1)*X(i)/X(i-1)

- otherwise t(i) = t(i-1)

- R(i) = xMA(i,t,N)

On Balance (Cumulative) Volume (OBV)

Indicator Type

Volume, Money Flow

Description